- Trillions of dollars in tax breaks enacted by former President Donald Trump are scheduled to expire after 2025 if Congress doesn't take action.

- The law included lower federal income tax brackets, bigger standard deductions and higher gift and estate tax exemptions, among other provisions.

- In the meantime, financial planners are advising clients on how to prepare.

With trillions of dollars in tax breaks scheduled to expire after 2025, financial advisors are working with clients to prepare for the looming tax cliff.

Enacted by former President Donald Trump, the Tax Cuts and Jobs Act of 2017, or TCJA, included lower federal income tax brackets, bigger standard deductions and higher gift and estate tax exemptions, among other provisions.

If Congress doesn't take action, those tax breaks will sunset after 2025. And if the TCJA provisions expire, more than 60% of tax filers could face increased taxes, according to the Tax Foundation.

Get Philly local news, weather forecasts, sports and entertainment stories to your inbox. Sign up for NBC Philadelphia newsletters.

While the expirations are roughly 18 months away, "now is the time for clients to be focused on the fundamentals of tax planning," said certified financial planner Jim Guarino, managing director at Baker Newman Noyes in Woburn, Massachusetts.

More from Personal Finance:

80% of Americans say grocery costs have increased since the pandemic started

Here's how to get lower interest rates without waiting on a Fed rate cut

IRS unveils plan to close 'major tax loophole' used by large partnerships

Of course, with control of Congress and the White House uncertain, it's difficult to predict which TCJA provisions, if any, could be extended.

Money Report

Still, without advanced preparation, some taxpayers could have to resort to "Hail Mary planning" at the end of 2025, said Guarino, who is also a certified public accountant.

Here are some tax strategies advisors are discussing with their clients.

Consider 'accelerating income'

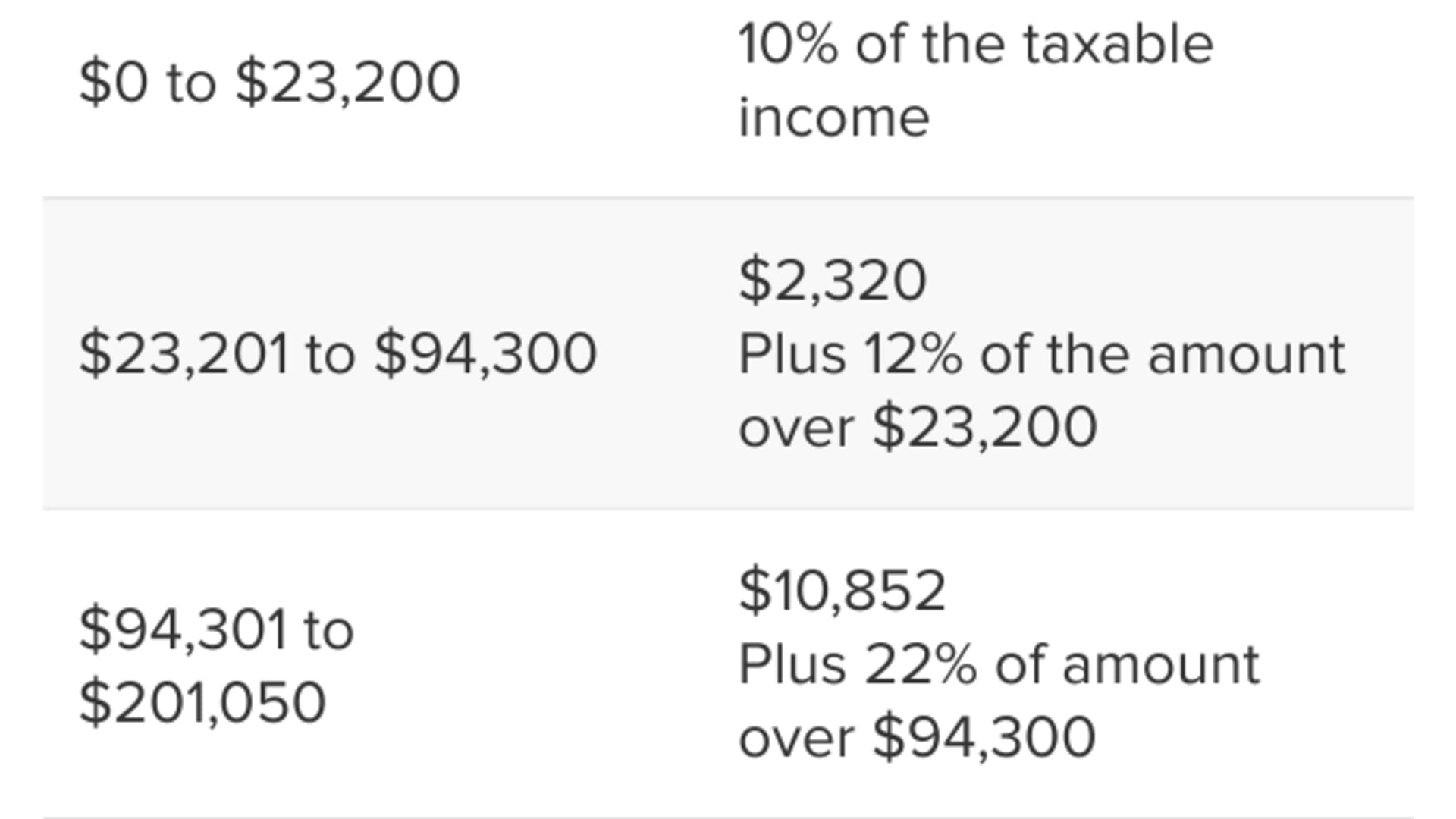

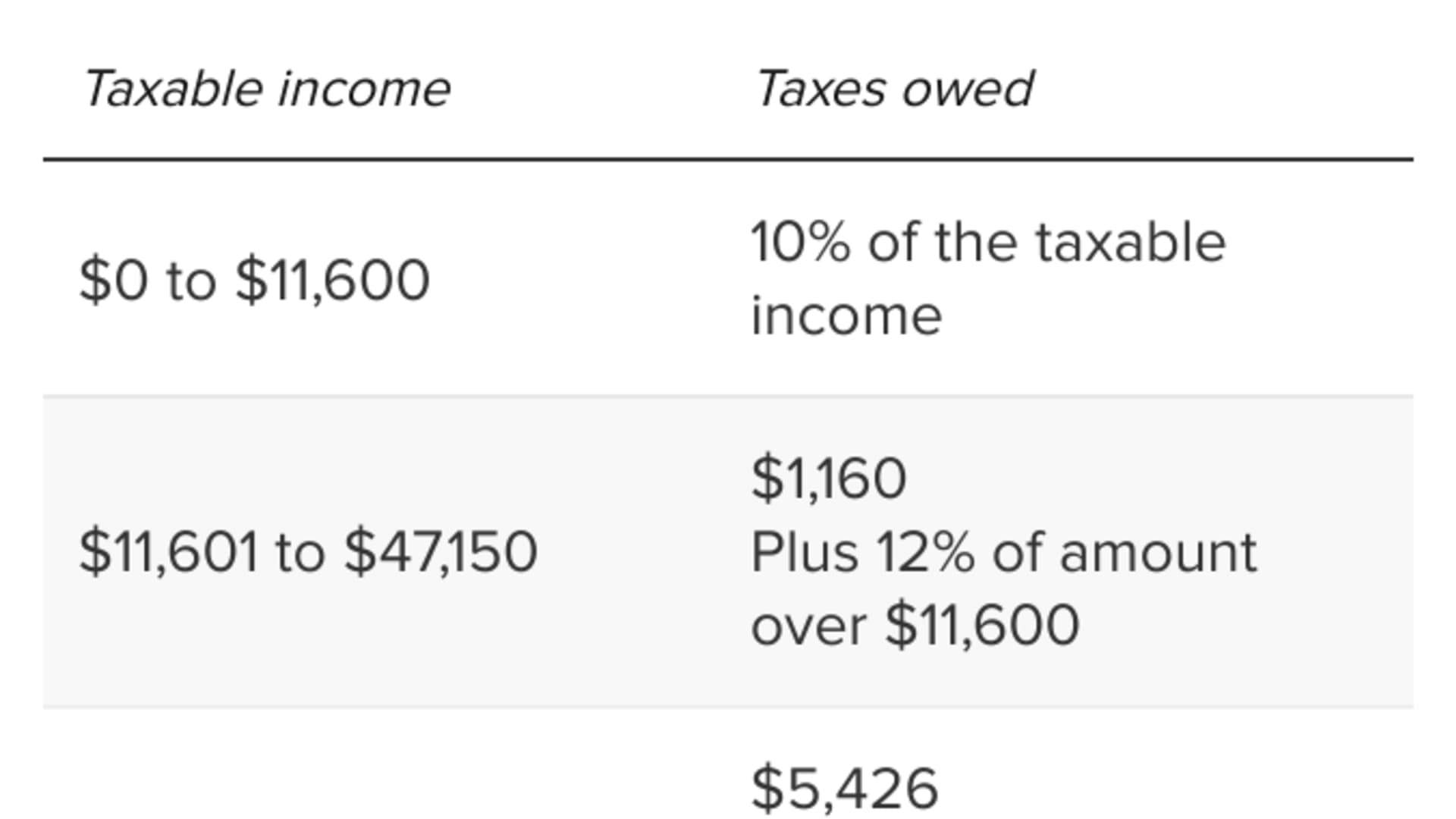

The TCJA temporarily lowered federal income tax rates, which dropped the top rate from 39.6% to 37% through 2025. In the meantime, you could consider "accelerating income" before 2025 to maximize lower rates and expanded brackets, Guarino said.

For example, some retirees may take early or increased pre-tax retirement account withdrawals that are "above and beyond" their required minimum distributions, he said.

Another way to leverage temporary lower tax brackets is through so-called Roth individual retirement account conversions, according to CFP Nayan Lapsiwala, director of wealth management and partner at Aspiriant in Mountain View, California.

You can use the strategy to transfer pre-tax or non-deductible IRA funds to a Roth IRA for future tax-free growth. While the converted balance incurs upfront levies, your bill is typically smaller in lower tax years.

However, before incurring extra income, you need to weigh how increased earnings could trigger the so-called net investment income tax or affect phaseouts for tax deductions or credits, Guarino warned.

Plus, with added income, you'll typically need to make quarterly tax payments to avoid underpayment penalties, he said.

Weigh 'lifetime gifts' for large estates

The temporary raised gift and estate tax exemption is a key provision for high-net-worth families, experts say.

Adjusted for inflation, the exemption rose to $13.61 million per individual or $27.22 million for married couples in 2024. But those limits will drop by roughly half after 2025.

"Nobody can control when they die, but there are benefits to making lifetime gifts," said Jane Ditelberg, director of tax planning for Northern Trust in Chicago.

Individuals or married couples can remove assets from their estate by making lifetime gifts before the higher thresholds expire.

"But it really only applies to those people who are in a position to make a gift of more than $7 million," Ditelberg said.