- If you're eyeing a year-end Roth individual retirement account conversion, you'll need to plan for the upfront tax bill.

- When you complete a Roth conversion, you'll owe regular income taxes on the converted balance, based on your current-year taxable income.

- Typically, it's better to cover taxes with funds outside the conversion, experts say.

If you are considering a year-end Roth individual retirement account conversion, you'll need to plan for an upfront tax bill.

Roth conversions move pretax or nondeductible IRA funds to a Roth IRA, which can kick-start tax-free growth. It's a popular strategy among investors with large pretax balances, particularly in lower-income years, experts say.

Still, "it can be hard to bite the tax bullet today and do a Roth conversion," said certified financial planner Abrin Berkemeyer, a senior financial advisor with Goodman Financial in Houston.

Get top local stories in Philly delivered to you every morning. >Sign up for NBC Philadelphia's News Headlines newsletter.

When a Roth conversion is completed, you'll owe regular income taxes on the converted balance, based on your current-year taxable income.

Ideally, you're "managing the tax bracket," said CFP Jim Guarino, managing director at Baker Newman Noyes in Woburn, Massachusetts. He is also a certified public accountant.

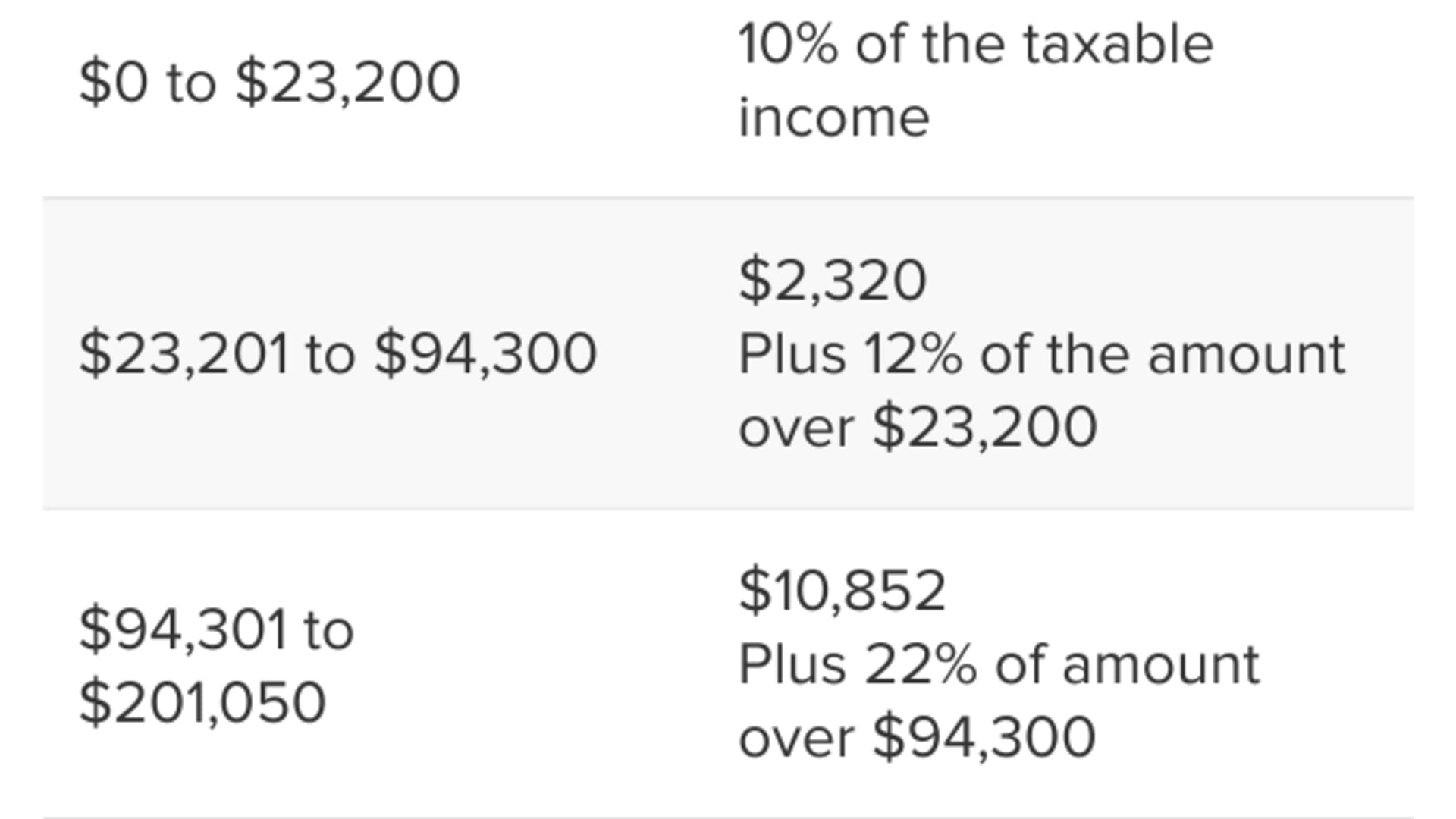

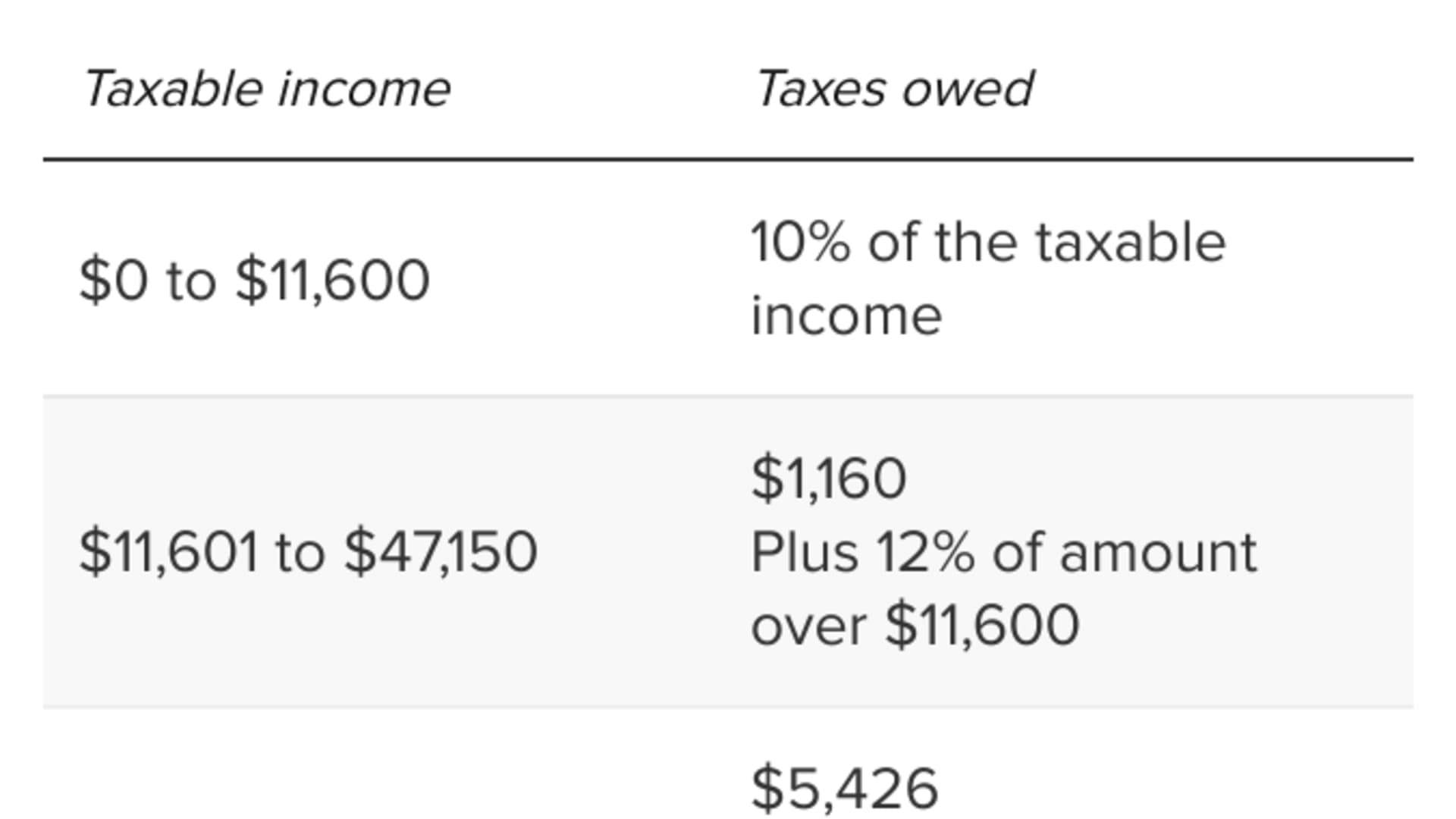

That could involve partial conversions by incurring only enough income to stay within a specific tier. For 2024, there's a small increase from 10% to 12% or 22% to 24%, but a larger jump from 24% to 32%, Guarino explained.

Ideally, you will want a conversion that keeps you comfortably within a tax bracket, meaning you can afford the upfront bill, Guarino said.

Money Report

Of course, Roth conversion strategies depend on clients' long-term goals, including estate planning, experts say.

How to pay for taxes on your Roth conversion

Typically, it's better to cover the upfront taxes with other assets, rather than using part of the converted balance to cover the bill, Berkemeyer said.

The more funds you get into the Roth, the higher your starting balance for future compound growth to "get the maximum benefit out of the conversion," he said.

Cash from a savings account is one of the best options to pay for taxes, Berkemeyer said. However, you can also weigh selling assets from a brokerage account.

Something to consider if you're selling brokerage assets to pay Roth conversion taxes: If it's a lower-income year, you could qualify for the 0% long-term capital gains bracket, assuming you've owned the investments for more than one year, he said.

For 2024, you may qualify for the 0% capital gains rate with a taxable income of up to $47,025 if you're a single filer or up to $94,050 for married couples filing jointly.

However, you'd need to run a projection since the Roth conversion adds to your taxable income.